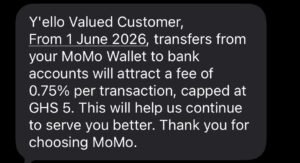

MTN Ghana has announced that from June 1, transfers from MoMo wallets to bank accounts will attract a 0.75% fee, capped at GH¢5 per transaction a move that is already triggering intense debate across Ghana’s financial and digital economy space.

In an SMS notification sent to subscribers, the telecom giant explained that the new charge is aimed at helping the company “serve customers better.” But beyond the official explanation, the decision is being interpreted by many analysts as a significant signal in the growing rivalry between telecom-driven financial platforms and traditional banks.

What appears on the surface to be a standard service fee could, in reality, influence how millions of Ghanaians choose to store, transfer, and manage their money.

Over the years, MTN MoMo has evolved far beyond a simple mobile transfer service. Today, it operates as one of Ghana’s most influential financial ecosystems, handling transaction volumes that rival some traditional banking institutions.

For many users, especially within Ghana’s informal economy, MoMo has effectively become a digital bank account, supporting payments, savings, lending, insurance, merchant settlements, and everyday business transactions.

However, a major behavioral pattern has long existed: customers often receive money in their MoMo wallets and quickly transfer those funds into bank accounts for savings, withdrawals, or larger business transactions.

With the introduction of the new transfer fee, financial observers believe that pattern could begin to change.

If transferring money from MoMo to a bank account becomes more expensive, users may choose to keep more funds inside their wallets instead. That shift could significantly strengthen the MoMo ecosystem by increasing wallet balances and deepening customer dependence on mobile money platforms.

The development is also reigniting conversations about the growing competition between banks and fintech-led telecom services.

Some industry watchers argue that MTN’s decision may partly reflect years of bank charges imposed on customers moving money from bank accounts into mobile wallets. In many cases, banks have charged users for bank-to-wallet transfers, while wallet-to-bank transfers remained largely free.

This has led some analysts to question whether MTN’s latest move is less about introducing a new burden and more about creating what they describe as “competitive symmetry” in Ghana’s financial ecosystem.

If banks charge customers to move money into wallets, should telecom wallets not also charge customers moving money back into banks?

That question now sits at the center of what many believe is a broader battle over transaction flows, customer liquidity, and ultimately, who controls where Ghanaians keep their money.

The comparison to the now-abolished E-Levy has also quickly surfaced online.

Technically and legally, the two are completely different. The E-Levy was a government-imposed tax on electronic transfers, while this new charge is a private commercial fee introduced by a telecom operator.

Yet psychologically, the memories may feel similar for many users.

The E-Levy was scrapped partly to reduce barriers to digital transactions and encourage electronic payments. Now, only months later, another fee is emerging within one of Ghana’s most widely used digital payment channels.

While this new charge is not a tax, it may revive concerns among consumers about the rising cost of digital financial transactions.

Ultimately, the real significance of MTN MoMo’s latest decision may go far beyond the 0.75% fee itself.

The development highlights a rapidly evolving financial landscape where the competition is no longer simply between telecom companies. Increasingly, the real battle appears to be between traditional bank accounts and digital wallets between conventional banking institutions and platform-based financial ecosystems fighting for customer trust, liquidity, and long-term dominance in Ghana’s economy.

Tap Here For More News Updates